Table of Contents

Introduction

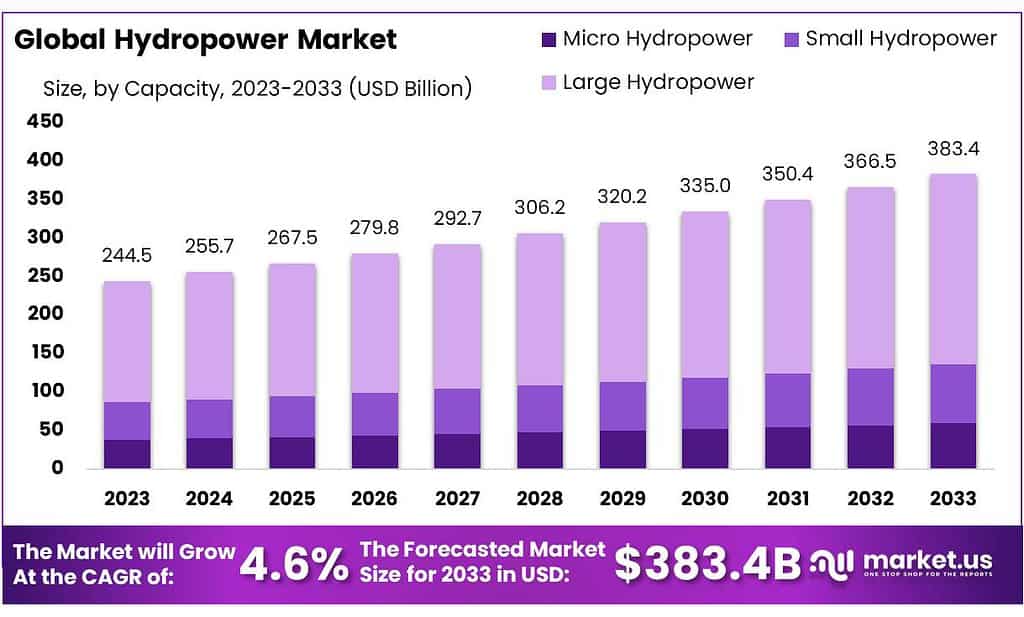

The global hydropower market, expected to reach a value of USD 383.4 billion by 2033 from USD 244.5 billion in 2023, is anticipated to grow at a compound annual growth rate (CAGR) of 4.6% over the forecast period from 2023 to 2033. This growth is driven by various factors, including the increasing demand for clean and renewable energy, advancements in hydropower technology, and supportive government policies aimed at reducing carbon emissions.

Hydropower, which leverages the kinetic energy of moving water to generate electricity, remains a cornerstone of renewable energy strategies worldwide. Its ability to provide a stable and reliable power supply makes it an attractive option for meeting rising global energy demands while contributing to sustainability goals. In 2023, hydropower capacity grew by 13.5 GW to 1,412 GW, with significant contributions from pumped storage hydropower, which increased by 6.5 GW to 182 GW.

Key growth drivers for the hydropower market include the need for cost-effective and sustainable energy solutions. Hydropower plants, particularly those incorporating pumped storage, offer essential grid stability and storage capabilities, which are increasingly important as the share of variable renewable energy sources like wind and solar grows. This is particularly relevant in regions with high renewable integration, where hydropower provides necessary balancing services.

However, the market also faces notable challenges. Environmental and social concerns related to large-scale hydropower projects, such as ecosystem disruption and displacement of communities, have led to stricter regulatory scrutiny and longer permitting processes. In advanced economies, declining electricity prices and uncertain long-term revenue streams have made new investments less attractive. Addressing these challenges through improved regulatory frameworks and innovative project designs is crucial for sustaining market growth.

Recent developments in the sector highlight both progress and areas needing attention. For instance, China remains the largest single market for hydropower, accounting for 40% of global capacity growth, though its pace has slowed due to environmental concerns and the scarcity of viable large project sites. Meanwhile, regions like Southeast Asia and Sub-Saharan Africa are witnessing faster growth, driven by increasing electricity demand and export opportunities. Notably, China’s involvement in financing and constructing hydropower projects in these regions underscores its significant role in global market expansion.

Key Takeaways

- Market Growth Expected to reach USD 383.4 billion by 2033 from USD 244.5 billion in 2023, growing at a CAGR of 4.6%.

- The public segment captures over 85% market share, driven by government investments and a renewable energy focus.

- Facilities over 30 MW hold a 64.5% market share, supplying stable electricity to national grids.

- Reservoir technology dominates with a 54.6% share, while pumped storage and run-of-river solutions gain traction.

- Large Hydropower leads with a 64.5% share, followed by Small Hydropower and Micro Hydropower, catering to diverse energy needs.

- Asia Pacific leads with a 43.6% market share, driven by renewable energy demand and infrastructure development.

- Hydropower accounts for around 16% of the world’s total electricity generation.

- In 2023, the world’s tallest hydropower station, the Baihetan Dam in China, with a height of 289 meters, became fully operational.

Hydropower Statistics

- The installed capacity of hydropower rose to 1330 GW as of 2020 and is expected to grow at a CAGR of 1.93% to 1520 GW by 2027.

- Capital costs currently make up 80-90% of hydropower costs.

- The average amounts to around 2% of initial investment costs.

- India recently moved up the ranks, taking Japan’s spot, as the fifth largest hydropower producer with over 100 plants averaging above 25 MW each.

- China is predicted to remain the single largest source of hydropower up until 2030, responsible for 40% of global supply.

- According to the US Energy and Information Administration, 7.3% of utility-scale electricity in the United States is produced from hydropower, representing a substantial contribution to the US renewable electricity mix (all other forms of renewable generation account for 12.5% with wind and solar representing 8.4% and 2.3%, respectively).

- Hydropower accounts for 60% of all renewable sources and 16% of total electricity generation, with this number higher than 90% in countries like Albania, Congo, Ethiopia, Nepal, Norway, and Paraguay.

- Renewables (predominantly wind and solar resources) account for 9%, while hydropower accounts for an additional 7% of the electric energy generation in ISONE.

- Renewable energy makes up 28.1% of the world’s electricity production

- Norway is followed by New Zealand at 80.9%, Brazil at 78.4%, Colombia at 74.5%, and Canada at 68%. Brazil’s high renewable capacity is due primarily to the significant number of hydropower stations in the nation’s rivers.

- The percentage of renewable energy consumption in Latin America was even higher, at 61.6%.

- Europe comes in second with 40.7% of all energy generation through renewable sources.

- By 2027, projections indicate renewables will account for more than 90% of all global electricity expansion efforts.

- While China is the largest producer of renewable energy, it accounts for only 28.8% of all energy production in the country. However, it’s still number one in Asia, followed by India where 20.4% of energy production is from renewable sources.

- In South America, Brazil is number one with 78.4% of their energy generation from renewable sources.

- Powering Non-Powered Dams (NPD) are existing dams that do not currently have hydropower. Previous studies have estimated up to 12 GW of technical potential of U.S. NPD based on an average monthly flow rate over 30 years and a design flow rate exceedance level of 30% at more than 54,000 dams in the contiguous United States.

- NSD CAPEX is reduced by 5% in 2035 and 8.6% in 2050.

- NPD CAPEX for 2026 to 2030 and 2031 to 2040 are, respectively, 5% and 10% lower than the Moderate Scenario for 2030.

- All NSD CAPEX reduced 30% in 2035 and 35.3% in 2050. This is consistent with the Advanced Technology case in the 2016 Hydropower Vision study.

- Hydropower provides 31.5% of the country’s renewable electricity (and 6.3% of its total electricity). Nearly every state uses it.

- the Bipartisan Infrastructure Law invests more than $700 million in existing hydropower facilities to improve efficiency.

- By 2050, U.S. hydropower capacity could grow by about 50%, increasing to 150 gigawatts.

- That much renewable energy could power more than 35 million average U.S. homes, save $200 billion from avoided greenhouse gas emissions and require a workforce of nearly 200,000 people in hydropower-related jobs.

Emerging Trends

- Technology Upgrades: Innovations in turbine technology are enhancing the efficiency and flexibility of hydropower plants. For instance, the development of permanent magnet generators and fish-friendly turbines is helping to increase power output while minimizing environmental impact. These technologies allow hydropower plants to operate efficiently across a wider range of hydraulic conditions.

- Digitalization: The integration of digital technologies is transforming hydropower operations. Real-time data collection and processing enable advanced grid-supporting services without compromising the reliability of the plants. Digital twin technology and real-time simulations are used to optimize plant operations and maintenance, leading to increased efficiency and reduced operational costs.

- Energy Storage Solutions: With the growing share of variable renewable energy sources like wind and solar, the role of energy storage in hydropower is becoming more critical. Pumped storage hydropower (PSH) is particularly important as it allows for the storage of excess energy and its release during peak demand periods. This capability enhances grid stability and supports the integration of other renewable energy sources.

- Modular Power Systems: Modular power generation systems are being developed to make the deployment and scaling of hydropower plants more efficient. These systems include advanced turbines and modular components that can be easily installed and maintained, thus reducing costs and improving flexibility. Technologies like gravity hydraulic machines and Archimedes screws are examples of such modular solutions.

- Environmental and Social Sustainability: Efforts are being made to mitigate the environmental and social impacts of hydropower projects. Innovations such as fish-friendly turbines and improved sediment management techniques are being implemented to reduce ecological disruptions. Additionally, community engagement and better regulatory frameworks are crucial for addressing social concerns related to hydropower development.

- Climate Resilience: As climate change affects water availability, hydropower plants are being adapted to operate under varying conditions. This includes the development of technologies that enhance plant flexibility and resilience to droughts and floods. Maintaining and modernizing aging infrastructure is also vital for ensuring long-term operational efficiency and reliability.

- Market and Policy Dynamics: The hydropower market is influenced by policy measures that provide revenue certainty and reduce investment risks. Long-term contracts and power purchase guarantees are essential for attracting investment. Additionally, supportive policies, such as tax credits and incentives for renewable energy projects, play a significant role in driving market growth.

- Global Expansion: Hydropower development is expanding in regions with high untapped potential, such as Southeast Asia, Sub-Saharan Africa, and Latin America. These areas are seeing increased investment and project development due to rising electricity demand and the availability of suitable sites. China remains a major player, contributing significantly to global capacity additions.

Use Cases

- Large-Scale Power Plants: Large hydropower plants, such as the Three Gorges Dam in China, contribute significantly to national grids. The Three Gorges Dam has an installed capacity of 22.5 GW, making it the largest hydropower plant in the world. It generates approximately 100 TWh of electricity annually, enough to power 70 million households.

- Grid Support: Hydropower plants provide essential grid stability by quickly adjusting output to match demand. For example, the Hoover Dam in the United States, with a capacity of 2.08 GW, is used to balance supply and demand on the grid, especially during peak hours.

- Pumped Storage Hydropower (PSH): PSH systems store energy by pumping water to a higher elevation during low-demand periods and releasing it to generate electricity during peak demand. The Bath County Pumped Storage Station in Virginia, USA, is one of the largest PSH facilities, with a capacity of 3 GW. It plays a critical role in balancing the grid and providing emergency power.

- Flexibility and Reliability: PSH enhances the flexibility and reliability of renewable energy systems by storing excess energy from sources like wind and solar and releasing it when needed, thus ensuring a stable power supply.

- Small and Micro Hydropower: Small-scale hydropower projects are essential for providing electricity to rural and remote areas. For instance, Nepal utilizes micro-hydropower plants to supply electricity to remote villages, improving the quality of life and supporting local economies. These plants typically range from 5 kW to 100 kW and are crucial in areas not connected to the national grid.

- Economic Development: Access to reliable electricity from small hydropower plants enables local industries, such as agriculture and small-scale manufacturing, thereby fostering economic development in remote regions.

- Flood Control and Water Management: Hydropower dams often serve multiple purposes, including flood control, irrigation, and water supply. The Aswan High Dam in Egypt, for example, provides irrigation for millions of hectares of farmland and helps manage the Nile River’s flow, preventing floods and droughts.

- Recreational Opportunities: Many hydropower reservoirs are used for recreational activities such as fishing, boating, and tourism. The Hoover Dam’s reservoir, Lake Mead, attracts millions of visitors each year, boosting the local economy through tourism.

- Powering Industrial Operations: Industries located near hydropower plants benefit from the low-cost and reliable electricity supply. For example, aluminum smelting plants, which require large amounts of electricity, often rely on hydropower. The Alcoa aluminum plant in Tennessee, USA, utilizes electricity generated by the nearby hydropower plant on the Tennessee River.

- Sustainable Industrial Growth: Hydropower provides a sustainable and cost-effective energy solution for industries, reducing their carbon footprint and promoting greener industrial growth.

- Reducing Carbon Emissions: Hydropower is a clean energy source that significantly reduces carbon emissions compared to fossil fuels. It currently accounts for about 16% of global electricity generation and plays a vital role in mitigating climate change by avoiding approximately 3 billion tonnes of CO2 emissions annually.

- Supporting Renewable Integration: By providing grid stability and storage solutions, hydropower supports the integration of other renewable energy sources like wind and solar, helping countries achieve their renewable energy targets and reduce dependence on fossil fuels.

Major Challenges

- Environmental Impact: One of the primary concerns with hydropower projects is their environmental impact. The construction of large dams and reservoirs can lead to the flooding of vast areas, resulting in the loss of wildlife habitats, agricultural land, and forests. For instance, the Three Gorges Dam in China, while generating significant power, displaced over 1.3 million people and submerged numerous towns and archaeological sites.

- Social Displacement: Large hydropower projects often necessitate the relocation of communities. This displacement can lead to social and economic disruptions, as people are moved from their homes and livelihoods. The displacement associated with the Narmada Dam in India has affected thousands of people, leading to long-standing social and legal battles.

- High Initial Costs: The development of hydropower plants requires substantial initial investment. Building dams, turbines, and associated infrastructure involves significant financial resources. For example, the Grand Ethiopian Renaissance Dam, currently under construction, has an estimated cost of around USD 4.8 billion. These high upfront costs can be a barrier to the development of new projects, especially in developing countries.

- Regulatory and Permitting Challenges: Obtaining the necessary permits for hydropower projects can be a lengthy and complex process. Regulatory requirements often involve extensive environmental and social impact assessments, which can delay project timelines. In Europe and North America, the permitting process for new projects can take several years due to stringent environmental regulations.

- Climate Change Impacts: Climate change poses a significant risk to hydropower production. Changes in precipitation patterns, increased frequency of droughts, and altered river flows can reduce the reliability of water resources needed for hydropower. In recent years, hydropower generation in regions like North America and Europe has been affected by prolonged droughts, highlighting the vulnerability of this energy source to climatic variations.

- Aging Infrastructure: Many existing hydropower plants are aging and require significant investments for modernization and maintenance. Approximately 40% of the global hydropower fleet is over 40 years old. Upgrading these plants is essential to maintain their efficiency and safety, but it also involves substantial costs and logistical challenges.

Market Growth Opportunities

- Technological Innovations: Advancements in hydropower technology, such as the development of fish-friendly turbines and digital twin technology, enhance the efficiency and environmental sustainability of hydropower plants. For instance, digitalization can optimize operations and maintenance, potentially adding up to 42 TWh of additional energy production annually, resulting in operational savings of USD 5 billion per year.

- Pumped Storage Hydropower (PSH): PSH remains a key growth area due to its ability to store energy and provide grid stability. As the integration of intermittent renewable energy sources like wind and solar increases, the demand for reliable storage solutions like PSH is rising. The International Energy Agency (IEA) forecasts significant growth in PSH capacity, which is essential for balancing supply and demand in the power grid.

- Expansion in Emerging Markets: Developing regions such as Southeast Asia, Sub-Saharan Africa, and Latin America offer substantial growth opportunities due to their untapped hydropower potential. Countries like Nepal and Laos are developing projects to export electricity, driven by increasing regional demand and favorable investment conditions. China’s involvement in financing and constructing these projects further boosts growth prospects in these regions.

- Modernization of Aging Infrastructure: Many hydropower plants worldwide are over 40 years old and require modernization to maintain efficiency and safety. Upgrading these facilities with modern technologies can significantly enhance their performance and extend their operational life. This presents a lucrative market opportunity for companies specializing in retrofitting and upgrading existing hydropower plants.

- Government Policies and Incentives: Supportive government policies and financial incentives are crucial drivers for hydropower development. For example, the U.S. Inflation Reduction Act of 2022 provides tax credits and other financial incentives for renewable energy projects, including hydropower. Such policies reduce investment risks and attract private sector participation,

- Climate Change Mitigation: Hydropower’s role in reducing carbon emissions and combating climate change creates growth opportunities. As countries strive to meet their climate targets, investments in renewable energy, including hydropower, are increasing. Hydropower currently accounts for about 16% of global electricity generation and avoids approximately 3 billion tonnes of CO2 emissions annually, highlighting its importance in global energy strategies.

Recent Developments

China Three Gorges Corporation (CTG), the world’s largest hydropower developer, has demonstrated remarkable achievements in the hydropower sector throughout 2023 and early 2024. In 2023, the Three Gorges Dam generated over 80.2 billion kWh of electricity, marking a 1.88% year-on-year increase despite challenging inflow conditions that were 24% lower than the long-term average. Monthly cargo throughput via the dam’s ship locks also set records, with August 2023 seeing over 15.71 million tonnes of cargo, contributing to a total annual throughput of 172.34 million tonnes, a 7.95% increase from the previous year. In the first quarter of 2024, the dam reported a cargo throughput of 30.2 million tonnes, maintaining smooth operations even under severe weather conditions and maintenance activities. These milestones underscore CTG’s continued leadership in hydropower generation and its critical role in supporting China’s energy and transportation infrastructure.

Electricité de France (EDF) remains a major player in the hydropower sector, demonstrating significant operational performance in 2023 and early 2024. In 2023, EDF’s hydropower production reached approximately 58.8 TWh, showing a strong recovery compared to the previous year, thanks to more favorable hydrological conditions that allowed for higher reservoir levels. Monthly data from 2023 indicates that hydropower generation was particularly robust in the spring and early summer months, with peak outputs in May and June due to increased water availability from snowmelt and rainfall.

State Power Investment Corporation (SPIC) has been actively enhancing its role in the hydropower sector through the development and operation of significant hydropower projects in 2023 and 2024. In 2023, SPIC’s hydropower plants achieved notable operational milestones. The company’s total hydropower generation for the year was substantial, reflecting its commitment to renewable energy and sustainability. Monthly data from 2023 indicates consistent performance, with peak outputs typically observed during the spring and early summer months due to favorable hydrological conditions.

Duke Energy Corporation has made significant strides in the hydropower sector in 2023 and early 2024, continuing its commitment to clean and renewable energy sources. In 2023, Duke Energy’s hydropower plants played a crucial role in the company’s overall energy mix, contributing to its goal of reducing carbon emissions. Duke Energy’s hydropower generation throughout the year showed robust performance, particularly in the spring and summer months when water flow conditions were optimal.

Conclusion

Hydropower remains a cornerstone of the global renewable energy landscape, contributing significantly to reducing carbon emissions and stabilizing electricity grids. The sector’s growth is driven by technological advancements, government policies, and the pressing need for sustainable energy solutions to meet net-zero targets by 2050. However, challenges such as environmental impacts, aging infrastructure, and the need for substantial investment remain. To achieve the necessary expansion, approximately 26 GW of new capacity must be added annually until 2030, with further acceleration required thereafter. Hydropower’s ability to mitigate the effects of droughts and provide reliable, emissions-free energy underscores its importance in the global energy transition.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)