Table of Contents

Introduction

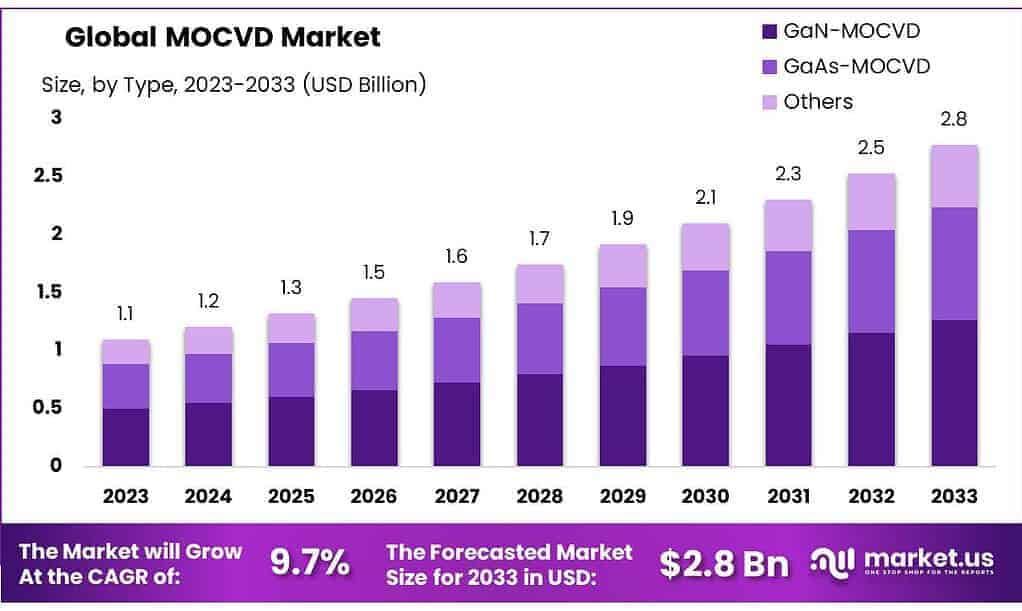

The global Metal Organic Chemical Vapor Deposition (MOCVD) Market is forecasted to grow substantially, expected to rise from USD 1.1 Billion in 2023 to approximately USD 2.8 Billion by 2033, demonstrating a robust Compound Annual Growth Rate (CAGR) of 9.7%. This market growth is fueled by several key factors, including technological advancements in semiconductor processes, increased demand for energy-efficient LED lighting, and the expanding semiconductor market.

The market’s demand is heavily supported by the surging need for high-performance electronic and optoelectronic devices across multiple sectors, such as consumer electronics, automotive, and telecommunications. MOCVD technology’s ability to deposit high-quality, high-performance material layers makes it integral to manufacturing semiconductors, LEDs, and photovoltaic cells, which are pivotal in today’s technology landscape.

Opportunities for market expansion are particularly pronounced in the development of power electronics and the continuous push for energy-efficient solutions. The Asia Pacific region leads this demand, attributed to its booming electronics and automotive sectors, coupled with significant investments in semiconductor manufacturing, especially in countries like China, South Korea, and Japan. This regional market dominance is supported by a growing consumer base and an increase in local manufacturing capabilities.

Additionally, the MOCVD market is witnessing a significant trend towards the adoption of energy-efficient and sustainable technologies, such as LED lighting and renewable energy applications. This trend is further driving the demand for MOCVD in the production of devices that support these technologies.

However, the market faces challenges such as the high costs associated with MOCVD equipment and the technical expertise required for operation, which could restrain growth to some extent. Despite these barriers, the market is expected to continue growing, driven by ongoing technological innovations and the increasing adoption of advanced electronics globally.

Key Takeaways

- Market Growth: The MOCVD market is expected to reach USD 2.8 Billion by 2033, with a CAGR of 9.7% from 2023.

- Segment Dominance: GaN-MOCVD captured a 45.6% market share in 2023, favored for power electronics in automotive and telecommunications.

- Application Focus: LED Manufacturing holds 41.5% market share in 2023, meeting global demand for energy-efficient lighting.

- Consumer Electronics: Leads MOCVD usage with 36.8% market share in 2023, driven by demand for advanced electronics like smartphones.

- Regional Trends: Asia Pacific leads with a 55.4% market share in 2023, driven by demand from consumer electronics and automotive sectors.

MOCVD Statistics

- At 268 nm, the device’s peak responsivity is constant across a range of voltages. At 20 V bias, the maximal photo-response is 16 mA/W, with a 7% external quantum efficiency.

- Using MOCVD, the MSM UV photodetector has a Mg concentration of 0.48.

- The growth temperatures for MOCVD and MBE are around 1300 K and 1000 K, respectively.

- The buffer layers used in the MBE and MOCVD growth processes are thin GaN layers that are generated at 770 K.

- The substrate temperatures for normal device growth are greater than MBE and fall between 500 and 1500 degrees Celsius because MOCVD uses hot gas flow and surface chemical reaction.

- For the MOCVD samples, an AlN buffer layer was utilized, and 1040°C is a common growth temperature.

- Both MOCVD and MBE samples exhibit an increase in free carrier concentration at Mg values up to 1×1019 cm−3.

- The aforementioned observations demonstrate that deep donors are required to explain the compensatory behavior and the 2.9 eV recombination appearance in heavily Mg doped GaN produced by MOCVD.

- The following conditions are necessary for AlN development by HT-MOCVD: substrate temperature of 1550 K, operating pressure of 40 Torr, gas flow rate of 50 slm, and susceptor rotational speed of 400 rpm.

- Following showerhead adjustment, the thickness non-uniformity of GaN films produced at 600 °C improved from 5.14% to 1.86%.

- Growing crystalline GaN films at 600 °C confirms the viability of the ICP-MOCVD, which is crucial for (opto)electronic devices.

- The improvement of 1.86% in the corresponding non-uniformity brings it very close to the commercial MOCVD.

Emerging Trends

- Increased Adoption in Power Electronics: MOCVD technology is increasingly being used in the power electronics sector due to its ability to handle higher power and temperature conditions. This is crucial for developing efficient electronic devices like LEDs, photovoltaic cells, and high-voltage transistors.

- Growth in Solar Energy Applications: The shift towards renewable energy sources is boosting the demand for MOCVD in solar cell production. The technology is essential for creating highly efficient photovoltaic cells, which convert sunlight into electricity with improved efficiency.

- Advancements in Semiconductor Manufacturing: There’s a notable trend towards the miniaturization and integration of semiconductor devices, driven by the demand for more compact and powerful electronic devices. MOCVD plays a key role in the fabrication of these advanced semiconductors, enabling the production of high-quality thin films necessary for high-performance electronics.

- Rise of Micro-LEDs: The growing popularity of Micro-LED technology in display applications is another significant trend. MOCVD is critical for producing Micro-LEDs that offer better color performance and energy efficiency than traditional LEDs, making them ideal for next-generation screens and lighting solutions.

- Expanding Market in Asia Pacific: The Asia Pacific region is witnessing a rapid expansion in the MOCVD market, fueled by the local manufacturing boom and government subsidies. This region’s dominance is supported by the concentration of semiconductor manufacturing facilities, particularly in countries like China, South Korea, and Taiwan.

- Advancements in AI and IoT Applications: As artificial intelligence (AI) and the Internet of Things (IoT) technologies continue to evolve, there is an increased demand for high-performance semiconductor devices, which MOCVD is well-equipped to produce. This technology supports the manufacturing of components essential for AI-powered devices and IoT systems, enhancing their capabilities and efficiency.

- Innovation in Equipment Technology: Continuous innovation in MOCVD equipment technology is enabling more precise control over the deposition process. These improvements include advanced reactor designs and more accurate temperature and gas flow controls, which result in better uniformity and properties of the deposited layers. This trend is crucial for meeting the stringent requirements of modern semiconductor and electronics manufacturing.

Use Cases

- Optoelectronic Devices: MOCVD is critical in the production of optoelectronic components such as lasers, photodetectors, and LEDs. These devices benefit from the fine control of film composition and thickness that MOCVD offers, which is vital for the efficient function of optoelectronics.

- Power Electronics: Utilizing materials like gallium oxide, MOCVD plays a pivotal role in the development of power electronic devices. These devices are essential for applications requiring high voltage and power efficiency, including renewable energy technologies, electric vehicles, and 5G networks.

- Microelectronics: In microelectronics, MOCVD is used to deposit very thin layers of compound semiconductors essential for high electron mobility transistors (HEMTs) and other microelectronic structures. This application is crucial for enhancing the performance and efficiency of electronic devices.

- Solar Cells: MOCVD technology is employed in the manufacturing of solar cells, particularly those made from compound semiconductors. The ability to create uniform, high-quality films makes MOCVD an excellent choice for photovoltaic devices that convert sunlight into electricity.

- Advanced Research and Development: MOCVD is instrumental in advancing research and development in various semiconductor materials, such as gallium nitride (GaN) and silicon carbide (SiC). These materials are integral to next-generation electronic and optical devices, where MOCVD’s precision and scalability are crucial for innovative applications.

- Photonics and Fiber Optics: The technology is crucial for creating the high-quality, defect-free layers necessary for photonics and fiber optics applications. MOCVD enables the development of materials with specific optical properties, essential for components like waveguides and optical amplifiers used in telecommunications.

- Quantum Computing: MOCVD facilitates the growth of quantum dots and other nanostructures that are foundational for quantum computing. The precision control over material properties provided by MOCVD is vital for developing the quantum bits that perform computations in quantum computers.

Major Challenges

- Temperature Control and Measurement: One of the major hurdles in MOCVD processes is achieving and maintaining precise temperature control. Accurate temperature measurement is crucial because even small deviations can affect the quality and consistency of the deposited films.

- Material Quality and Dislocation Density: The quality of materials produced by MOCVD is often compromised by high dislocation densities, which can degrade the performance of semiconductor devices. Reducing these dislocations remains a challenge, particularly in materials like gallium nitride (GaN).

- Stress and Strain Management: In the growth of films, especially on mismatched substrates like silicon, managing stress and strain to prevent wafer curvature or cracking is a critical challenge. This issue becomes more pronounced with larger wafer sizes or when the films are thicker, as these conditions increase the mechanical stress within the materials.

- Reproducibility and Uniformity: Achieving reproducible and uniform growth across different batches and reactor setups is challenging. Variations in gas flow, pressure, and chemical reactions can lead to inconsistencies in the thickness and composition of the deposited layers.

- Doping Control: Precise doping of the films, necessary for creating semiconductors with desired electrical properties, is difficult. The volatility and reactivity of doping substances, combined with high temperatures and complex gas flows, complicate the achievement of uniform and controlled doping levels.

- Chemical Handling and Safety: MOCVD processes involve highly reactive and often toxic chemicals under high temperatures. Managing these materials safely, including storage, handling, and disposal, presents significant challenges. Ensuring worker safety and environmental compliance requires robust systems and procedures.

- Scalability and Cost: Scaling MOCVD processes from laboratory to industrial scale while controlling costs is a daunting task. The capital expenditure for MOCVD equipment is high, and operating costs related to energy consumption and source materials can be substantial.

- Integration with Other Processes: Integrating MOCVD with other semiconductor manufacturing processes can be complex. Compatibility issues, such as different thermal budgets and chemical sensitivities, require careful management to maintain process integrity and yield.

- Advanced Materials Challenges: As MOCVD is used to develop novel materials for advanced applications, such as two-dimensional materials and nanostructures, new challenges in material stability, interface control, and new chemical precursors arise.

- Environmental Impact: The environmental impact of MOCVD processes, particularly concerning the emission of volatile organic compounds (VOCs) and other hazardous materials, poses ongoing challenges for sustainability and regulatory compliance.

Market Growth Opportunities

- Renewable Energy Sector: The increasing focus on renewable energy is expected to drive demand for MOCVD technology. This technology is crucial for producing semiconductors used in solar cells and power electronics, essential for renewable energy systems like solar panels and electric vehicles.

- LED Manufacturing: LED manufacturing remains a dominant segment within the MOCVD market, largely due to the global shift towards energy-efficient lighting solutions. The push for LEDs, known for their longer lifespan and lower energy consumption, continues to boost the demand for MOCVD technology in this sector.

- Semiconductors and Advanced Packaging: There is a rising demand for high-performance semiconductor devices, which are increasingly used in various electronics and smart devices. MOCVD technology is integral to meeting these needs, especially as electronic devices continue to miniaturize and require more precise semiconductor layers.

- Regional Growth Opportunities: The Asia-Pacific region, in particular, is a major hub for MOCVD market growth, driven by robust semiconductor manufacturing activities in countries like China, South Korea, and Taiwan. North America and Europe also show substantial growth prospects, fueled by advancements in semiconductor and optoelectronic technologies.

- Micro-LED Development: Innovations in display technology, especially the development of micro-LEDs, present new growth avenues for the MOCVD market. These displays are used in sectors like consumer electronics and augmented reality, where superior performance characteristics are critical.

- Power Electronics: The need for efficient and compact power systems is escalating, particularly in sectors like renewable energy generation and electric vehicles. MOCVD technology supports the development of high-performance semiconductor materials that are integral to these systems.

- Investment Surge: As the semiconductor industry continues to grow, fueled by demand for advanced electronics, there is a notable surge in investments in semiconductor equipment, including MOCVD systems. This increased investment is likely to enhance the production capabilities and technological advancements within the sector.

- Technological Advancements: Continuous improvements in CVD equipment technology enhance the MOCVD market’s prospects. These advancements contribute to more precise and efficient manufacturing processes, essential for producing superior quality semiconductor films.

Recent Development

- AIXTRON SE is a leading provider of MOCVD systems, crucial for manufacturing III-V compound semiconductors like gallium nitride (GaN). AIXTRON’s technology is pivotal for creating high-quality semiconductors used in various high-tech applications. Their systems, including the advanced AIX R6, are designed for cost-effectiveness and high throughput, essential for large-scale production of LEDs and other semiconductor devices.

- Veeco Instruments Inc. specializes in manufacturing equipment for semiconductor and advanced material applications, including MOCVD systems for creating power electronics, LED lighting, and solar cells. Veeco’s technology supports the production of devices requiring precise material properties and is recognized for enhancing production scalability and improving material quality.

- ASM International N.V. offers deposition systems that cater to semiconductor manufacturing, providing tools essential for atomic layer deposition (ALD), plasma-enhanced chemical vapor deposition (PECVD), and MOCVD. Their equipment is used globally to produce advanced semiconductor materials vital for electronics and solar industries.

- Taiyo Nippon Sanso Corporation is a major provider of industrial gases and related equipment, including MOCVD systems. They serve a broad spectrum of industries with a focus on enhancing semiconductor production processes and improving the efficiency and quality of electronic materials.

- CVD Equipment Corporation designs, develops, and manufactures a range of equipment, including MOCVD systems, for the production of advanced materials. Their systems are utilized in the research and development as well as commercial production of semiconductors, nanomaterials, and other technologically significant materials.

- Tokyo Electron Limited supplies innovative semiconductor production equipment systems, including those used for MOCVD. They focus on supporting the fabrication of next-generation semiconductors and enhancing the efficiency of material deposition processes.

- Jusung Engineering Co. Ltd. is a leader in the design and manufacturing of semiconductor manufacturing equipment, including MOCVD systems. They provide technologies that are integral to the production of microelectronics and optoelectronics, catering to the needs of high-performance semiconductor production.

- Applied Materials, Inc. is a global leader in materials engineering solutions used to produce virtually every new chip and advanced display in the world. Their technologies include MOCVD systems that are critical for semiconductor and solar cell fabrication.

- Intelligent Epitaxy Technology, Inc. focuses on providing epitaxial technologies for semiconductor production, including MOCVD. Their products are essential for the development of sophisticated semiconductor devices.

- Northrop Grumman utilizes advanced material deposition technologies such as MOCVD in the production of components for aerospace and defense applications. Their use of cutting-edge technology ensures high performance and reliability in extreme conditions.

- IQE plc specializes in the manufacture of advanced semiconductor wafers, with MOCVD playing a crucial role in their production processes. Their products are used in a variety of high-tech applications, from consumer electronics to solar energy.

- EpiGaN nv, now part of Soitec, produces GaN-on-Si materials using MOCVD for power and RF electronics, enhancing device performance and energy efficiency in applications such as telecommunications and automotive.

- Xiamen Powerway Advanced Material Co. Ltd. offers a wide range of semiconductor materials, including those produced using MOCVD. They focus on providing high-quality materials for electronic and optoelectronic applications.

- Okmetic Oy is a supplier of advanced silicon wafers, also leveraging MOCVD technology to enhance the material properties of their products for the electronics industry, particularly for sensors and discrete semiconductors.

Conclusion

In Conclusion, The Metal-Organic Chemical Vapor Deposition (MOCVD) Market is positioned for robust growth driven by its essential role in producing high-quality, precise semiconductor materials. The market’s expansion is fueled by rising demands across various sectors, including renewable energy, advanced electronics, and LED manufacturing. As technology evolves and industries seek more efficient and sustainable solutions, MOCVD remains a pivotal technology, supporting advancements in semiconductor fabrication and offering substantial opportunities for innovation and development in the tech landscape.

This growth trajectory is supported by increased investments in semiconductor infrastructure globally, particularly in regions like Asia-Pacific, which dominates the market due to its significant semiconductor manufacturing activities. The future of the MOCVD market looks promising with a steady increase in applications and technological enhancements, positioning it as a key player in the broader push towards high-tech and energy-efficient solutions.